Rapid sell off SAF Tehnika on news

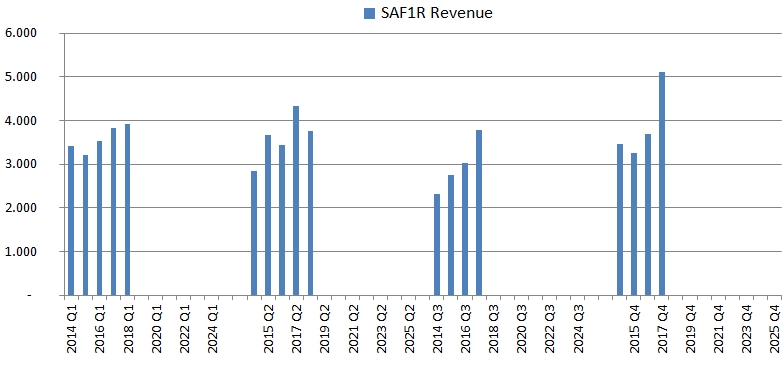

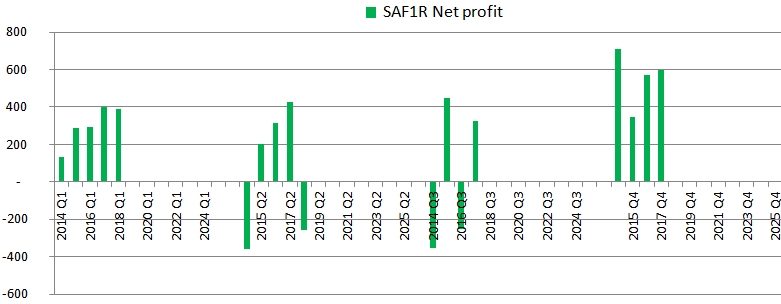

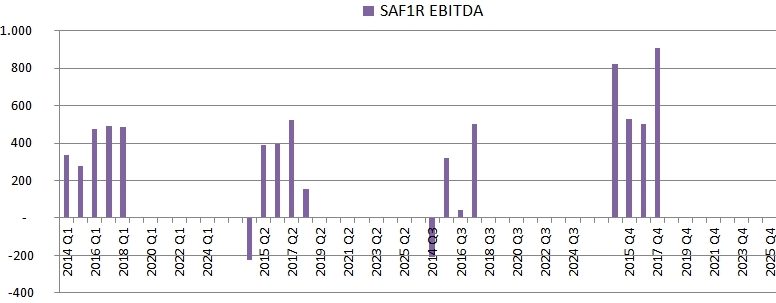

SAF Tehnika published their H1 FY result on the evening of February 7th. That evening I had time to quickly update my database and see what’s up with trailing numbers. So just a quick glance at SAF Tehnika 2017-2018 FY 6 months report:

Revenues for Q2 down -13.1% compared to Q2 of 2016-2017 FY.

Net loss amounted to -258k € with decreased EBITDA of over 3 times in Q2.

And just like that a gem in Baltic market became (at last price of H1 6.45 €):

- EV/EBITDA of 10.9;

- P/tBV of 1.9;

- and P/E of 18.3.

Previous trailing ratios can be found here.

Market reaction the next morning was adequate. I placed my ask that evening with a discount of -6%, but that was not sufficient and I had to exit at 6€ a share. I took a minimal profit of +2% including the received dividends from my recent additions and a sound +125% profit from 2016 acquisitions.

My suspicion was correct, and now SAF Tehnika trades at around 5.3€ a share.

SAF1R future

I do like this company. Clean balance sheet. High payout of dividends. Transparency.

Will definitely keep an eye on upcoming quarters. Management tends to point their business model, which is project type. It’s hard to even out quarters, and if Q2 was bad, maybe bunch of projects going to appear in Q3/Q4 which would make FY look reasonable. Will see how that goes.

Selling Silvano Fashion Group

I first bought SFG1T in 2015.06 at 1.41€ during the great turmoil with Russia invading Ukraine. Silvano has exposure to Russian ruble as well as tight trade relations to CIS region. Second purchase was just before publication the terrible financial report at 2.97€. Positions on the graph:

Including dividends early portion generated +146%, while a purchase 9 months back generated +6.9% profit or CAGR of +40.2% and +9.8% correspondingly.

SFG1T surprised market with gross 0.3 €/share dividends paid on last days of January 2018. I exited few days after ex-div date, taking dividends. Basic idea is to clear up portfolio a little bit. We are approaching the end of party in one way or the other. Better stay on the safe side. What I did not think through was upcoming general meeting, which will probably distribute more dividends. I suspect gross 0.1-0.15€ distribution per share. Will see. Share now trades at 2.77€.

Adding more INVL Baltic Real Estate

We have a flair of increasing inflationary pressure in Eurozone. Especially the Baltics. Commercial real estate contracts usually index their rental income with inflation, so in that way investing in real estate REIT is hedging against inflation.

Another thing is increased dividends. Together with Baltic Horizon Fund (REIT) portfolio exposure to commercial real estate now is about 30%.

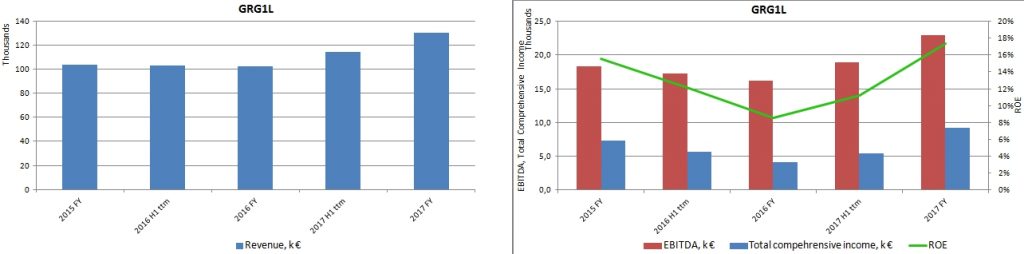

Adding Grigeo and purchase of East West Agro

At 1,42 I added more GRG1L to portfolio. Prior to purchase news came out on termination of agreement between Grigeo and Homanit Holding GmbH to purchase the sale of 100% of the shares of UAB Grigeo Baltwood. I expected this deal to improve Grigeo’s balance sheet and on one hand it was a negative announcement. However unaudited 2017 FY result was really really good. Quick peak:

Trailing EV/EBITDA decreased to 5.5 levels. Which is really good for this transparent company. For a long time GRG1L had negative free cash flow (FCF) due to endless investments. 2017 FY marked 17% FCF/Market Cap ratio. Which is promising on the dividend side. Debt burden also decreased and debt to equity ratio now stands at round 1.

Purchase of East West Agro (EWA1L)

Just a quick commentary. I think market beat down the price too much. I entered at 21.6. Q3 result wasn’t appealing, but I have reason to believe 2017 result will be far more satisfactory.

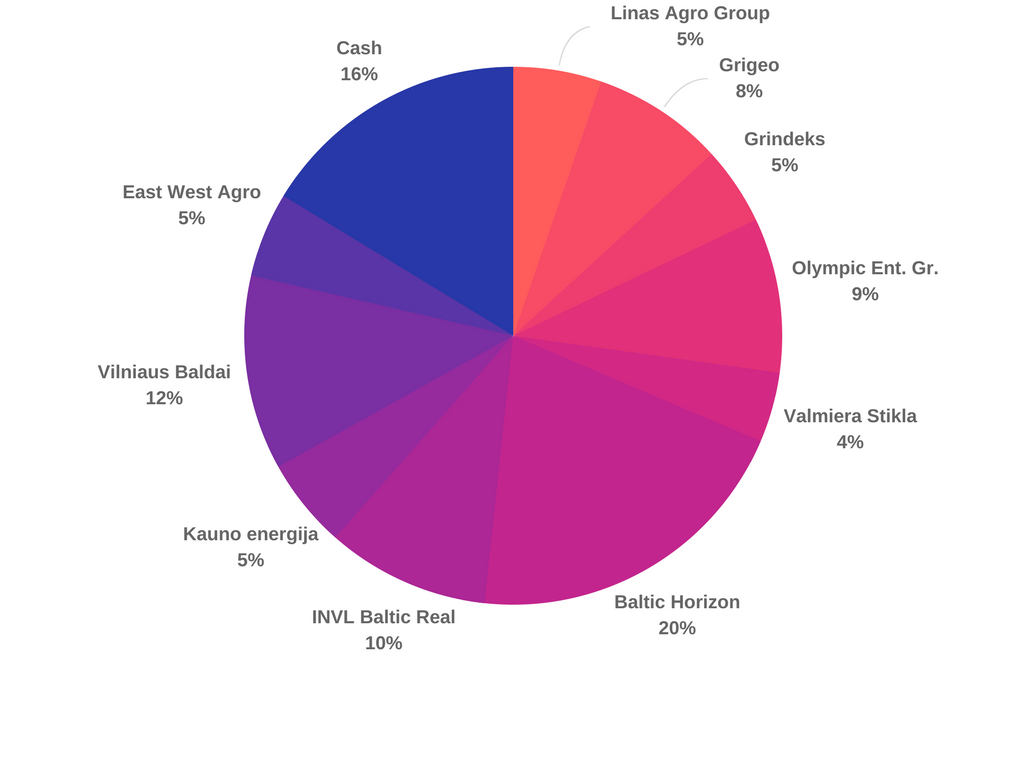

Current portfolio composition

As of 2018.03.17 with Friday’s prices my Baltic market portfolio structure looks like this:

You might also like

3 Comments

Hi there. Nice to find fellow Baltic investor 🙂 You got me interested in your largest REIT position. Since Im not able to buy US REITS its nice to find that there is a good Baltic REIT out there 🙂 BY the way what is your investment goal? Dividends or capital gain?

Hey p2035,

Baltic Market suggests 3 funds to invest in Baltic commercial real estate. EFT1T, INR1L and NHCBHFFT. Haven’t dug through EFEN fund really, as I just noticed during their IPO their dividend yield is lower than that of Baltic Horizon. Invalda Real Estate asset management and investment style is totally different. They purchase bargain deals, not in established well recognized objects.

Baltic Horizon Fund so far failed to deliver promised 8-9% annual return to unitholders, but at current market price and averaged trailing yield still holds at reasonably attractive 6.5% net yield. I think you should check them out. On Monday they are doing a webinar to present 2017 results. Feel free to ask further questions to the team itself 🙂 Few sentences more on my recent post:

https://goo.gl/oBYSZa

Concerning the strategy: I admire value investing philosophy with somewhat active approach of utilizing opening market opportunities, mainly in local (Baltic) market.

I see, so your not a dividend investors and our investing philosophies differ a lot and we might not understand what each saying to another 😀

Either way Baltic horizon looks quite atractive with well diversified RE units and main unit Europe PC you can visit 🙂 Actualy Europe PC is not the beat shoping center example but as long as it generates income will do. Thanks for showing me this fund. It might fill in the REIT gap that I got due to that stupif mifid2 regulations.

By the way your post updates are not visible on WP reader. Site is not based on WP platform?