Lagging on reporting

After I got back from Eurotrip I had been swamped by audited reports, Q1 data and plenty of other stuff. Two purchases of Auga Group were made in mid June and July, while entry to Harju Elekter was made during mid-June. Market setting has a bit changed and I’m not so enthusiastic about Harju Elekter entry, but charts below will help orient where I entered these Baltic equities.

Another entry to Auga Group

Last year I had Auga Group for a while, but the bull run without any particular reason let me to abandon the stock. The price topped at 0,645 and then checked local bottom at 0,462, at which I started rubbing my hands. Below is the chart of my entry to Auga Group points.

After the stock got back from the top I looked for reasons why it got there in the first place. I’ll write a more specific piece on AUGA SPO (second public offering) and expand there. Let’s just say I liked what I found and prior to announcement of SPO price I wanted to get a little stake of AUG1L. And got some at 0,48 €.

Few weeks later it was announced that SPO price range will be 0,45-0,5€ a share, which determined the price movement for the rest of July and mid-August. Retail investors should have made bids at SPO at maximum price (0,5€) so purchasing at the market seemed reasonable and I doubled my humble position once again at 0,484 €.

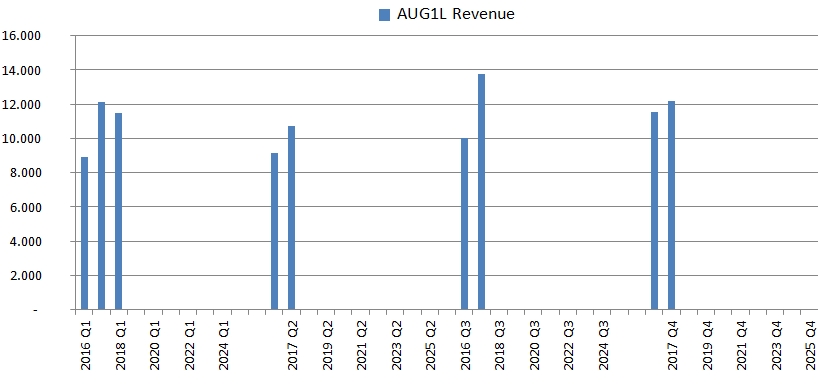

Glance at Auga Group Financials

Since I update my database each 6 months I can only provide trailing twelve months ratios for 2017 FY and last price (trading till the new shares are added to depositories is suspended) of 0,482:

- EV/EBITDA – 9,85;

- P/tBV – 1,16;

- P/E – 13,51;

- Debt/Equity – 0,88.

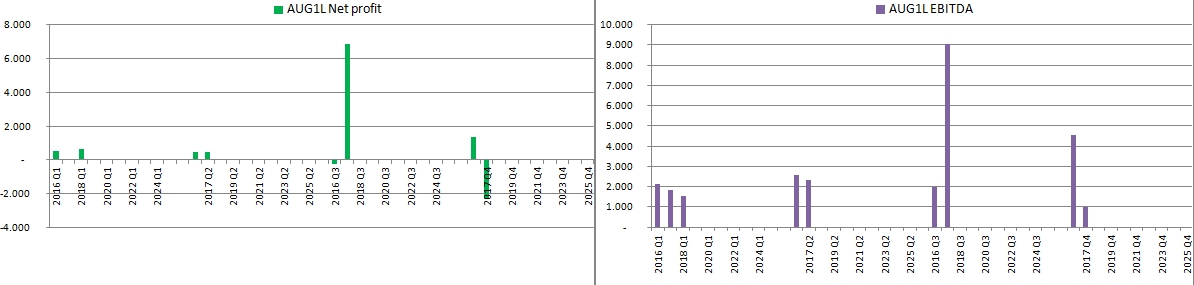

The Group also posted a mediocre 2018 Q1 with revenues -5,1% YoY change at 11 492 kiloeuros. Net profit of 625 and EBITDA of 1 560 k€, plotting that:

Graphic Auga Group Profits:

Note, that in 2017 Q3 revaluation of assets was made which contributed to one-off profit that bends charts a bit.

Revenues were lower due to longer organic grain delivery terms to clients than it was in previous year. For this reason larger part of deliveries will be done in upcoming quarters of 2018.

Considering a very dry summer results for 2018 might not be too good, but organic trend is on the rise and I’ll try to make a case for Auga Group in the next article. This small stake at AUGA that I made is more like FOMO, because I definitely don’t want to miss the ride.

Harju Elekter: Entry, Financials, Price Development, Dividends

I am actually uncomfortable talking about entry to Harju Elekter because market sentiment changed since I bought. However let me walk you through it. Here’s the Harju Elekter price performance of recent months and my entry point:

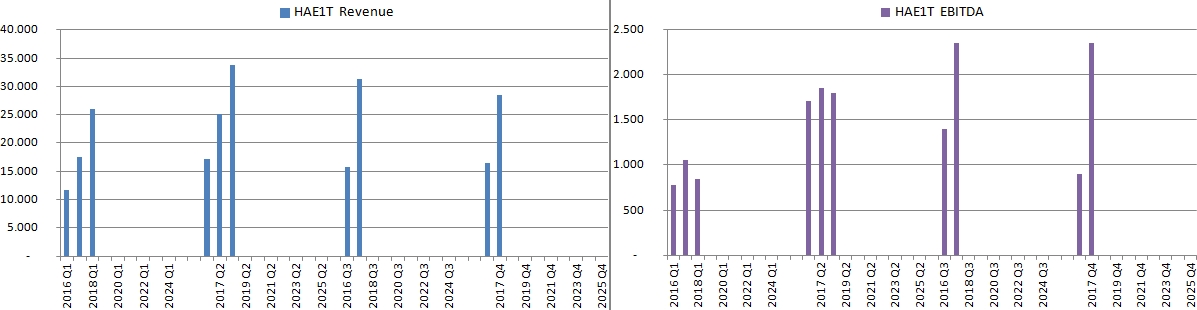

Now the brief story of price development is that Harju Group was expanding quite rapidly over the past several years. Price followed from 2,8 € at the end of 2016 to above shown levels. Harju Elekter already reported 2018 H1 figures so I can paint the picture for the last 3 years development in revenues and EBITDA:

As I mentioned first quarters disappointed the market and myself. Prior to buying I was inclined to think Q1 was a short bump. At least the EBITDA decline is not drastic. I don’t want to plot net profit, because in 2017 H1 Group sold a subsidiary for EUR 24M and this one-off item greatly distorts ratios, graphs and perhaps a mental picture of investors as well.

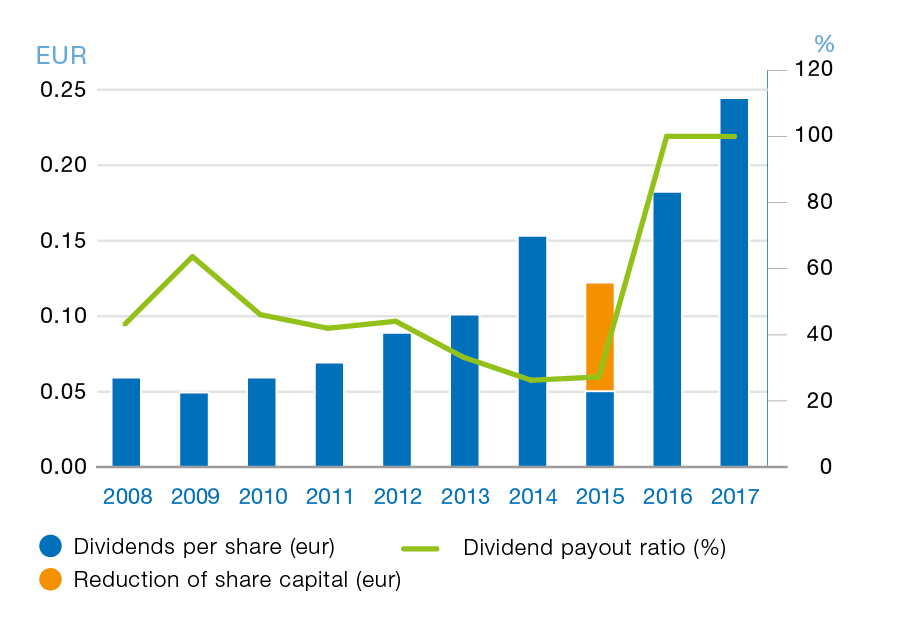

Harju Elekter Dividends 2018

Investors probably anticipated this 26M free cash flow to fall directly to dividends (hence the price topping at ~6,65€), but company paid out only EUR 4,2M (0,24€/share) which was still the record dividend payment for the Group.

Previous dividends and payout ratios, from Harju website:

As you can see the stock is a dividend cow. The problem is pricing.

Harju Elekter valuation for 2018 H1

Taking the price of 5,16€, for 2018 H1 most recent trailing twelve months data:

- EV/EBITDA – 12,65

- P/tBV – 1,54;

- P/E – 23,93;

- Debt/Equity – 0,47.

Another hidden argument for purchasing a stock at these ratios is Harju Elekter 10% stake at subsidiary Skeleton Technologies Group OÜ.

Skeleton Technologies

Skeleton Technologies is a leading European manufacturer of ultracapacitors – energy storage devices for short term, high tension output and saving. The more I dug about what they do and demand for their products the more reasonable unofficial guidance for 2020 of EUR 150M revenue looked.

Growth as depicted in this article is massive.

Skeleton, which has grown from the idea of the company, is today one of Europe’s leading manufacturers of energy storage devices. The company’s turnover grew three times last year

And in audited 2017 report Harju Elekter states:

The management of the Group assessed the fair value of ownership interest in the company on the basis of the price of new shares issued in the previous round of funding. The share of AS Harju Elekter decreased after the round of investment, dropping to 9.84%, while the recalculation of ownership interest increased the value of the financial investment by 1.6 million euros.

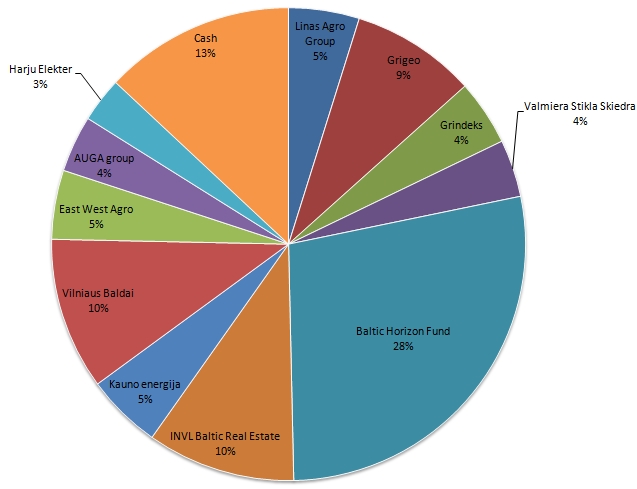

Portfolio Composition

Currently, with these recent additions, my baltic equities portfolio is very inclusive and as of 2018.08.23 looks like this:

You might also like

3 Comments

Hi! Why did you enter in the very moment when these stocks actually entered downtrend (sma100 & 200 cross)?

Hey Garry! I have plotted MA’s and SMA’s to clarify on what we are talking about.

Auga: https://goo.gl/k44TmP

Harju: https://goo.gl/VXS6ht

General answer – is that technical analysis works best in liquid markets. In Baltic Stock Market.. eh. Sometimes it does, sometimes it doesn’t. Over the years the significance of it on my actions in the market has decreased. I try to trade fundamental situation of a company in relationship to current/potential market sentiment.

On Auga’s case – you are absolutely right. Technically it would or I don’t know, maybe IS indicating a trend reversal right on my date range of purchases. As I mentioned in the article, company has really high ambitions and over the next 5 years might render all technical analysis worthless. Honestly, I did not use indicators while looking at the chart previous to purchase.

Harju – the cross happened post-purchase, so I couldn’t get this technical argument at the date of purchase. Q2 results were worse than I thought and it just might be the case, that the stock would mud the waters below 5euros for a while. However I’m cool with that, because it’s a dividend stock and any significant drop in price would result in demand of buyers targeting high yields. We still have to watch the fundamental trend though.

The second reason is that both stocks are below 5% in portfolio, which won’t hurt too much.

Cool. Was just curious. I usually use TA for timing, but I’ve never been a technical trader